Khushhali Sarmaya (Micro Enterprise Lending) Scheme 2024

Small business owners and micro-entrepreneurs often face financial challenges when it comes to scaling their businesses or managing working capital. To address these challenges, Khushhali Microfinance Bank offers the Micro Enterprise Lending. This loan is specifically designed to support micro-entrepreneurs in enhancing their production, purchasing inventory, and expanding their businesses.

In this article, we will provide an in-depth explanation of the Micro Enterprise Lending , covering its purpose, eligibility criteria, loan features, required documents, and the application process. By the end of this guide, all your questions will be answered, and you’ll know how to apply for the loan.

Read More : Khushhali Zamindar Loan Scheme Complete Guide for Farmers

What is the Khushhali Sarmaya (Micro Enterprise Lending) Loan Scheme 2024?

The Khushhali Sarmaya Loan Scheme 2024 is a loan facility aimed at micro-entrepreneurs—small business owners who need financial support to improve or expand their businesses. The loan can be used to purchase raw materials, finished goods, inventory, or business assets that are essential for generating income and increasing production.

This scheme is ideal for small businesses in need of working capital or investments in operating assets. With flexible repayment options and competitive loan amounts, the Khushhali Sarmaya Loan is designed to meet the specific needs of micro-entrepreneurs.

Key Features of the Khushhali Sarmaya Loan:

- Loan Amount: PKR 350,001 to PKR 1,000,000

- Tenure: 6 to 36 months

- Repayment Options: Equal monthly installments

- Collateral: Secured and unsecured options available

Whether you’re running a small retail shop, a manufacturing unit, or a service-based business, this loan offers the financial flexibility you need to take your business to the next level.

Read more : Khushhali Qarza Loan Scheme 2024

Purpose of the Khushhali Sarmaya Loan

The Khushhali Sarmaya Loan is designed to support micro-entrepreneurs by providing access to funds that can be used for various business purposes. Here’s how the loan can be used:

- Purchase of Raw Materials: Businesses can use the loan to buy raw materials that are essential for production or manufacturing processes.

- Inventory or Stock Purchase: Retailers or businesses that need to stock up on finished goods or inventory can use the loan to maintain or expand their stock levels.

- Enhancing Production: The loan can be used to upgrade or purchase new machinery, tools, or equipment to improve production capacity and efficiency.

- Business Expansion: Entrepreneurs looking to open new branches, expand their operations, or introduce new product lines can utilize the funds for these purposes.

This loan is highly flexible and can be tailored to the specific needs of each micro-entrepreneur, allowing them to invest in their businesses and increase their income.

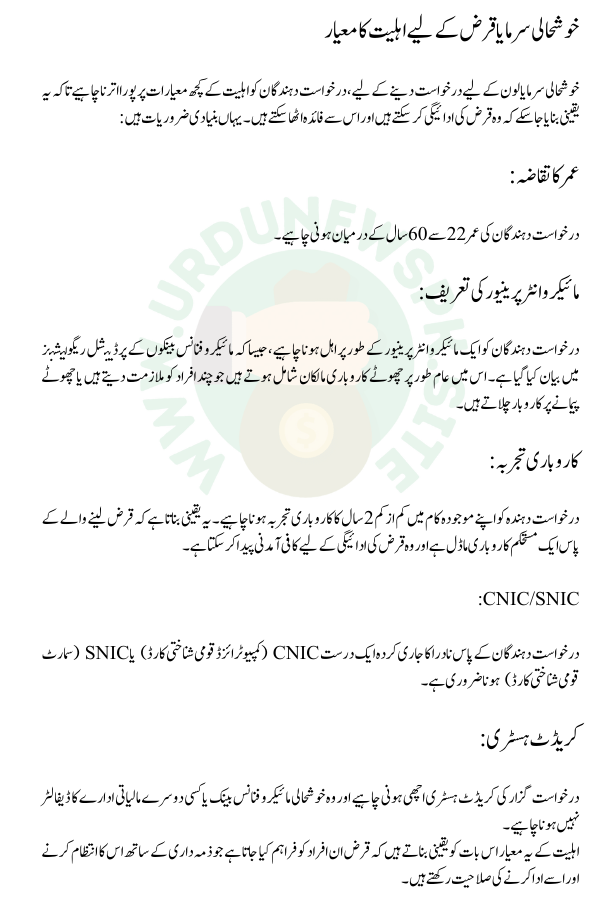

Eligibility Criteria for the Khushhali Sarmaya Loan

To apply for the Khushhali Sarmaya Loan, applicants must meet certain eligibility criteria to ensure they can repay the loan and benefit from it. Here are the basic requirements:

Age Requirement:

- Applicants must be between 22 and 60 years old.

Micro-Entrepreneur Definition:

- The applicant must qualify as a micro-entrepreneur, as defined in the Prudential Regulations for Microfinance Banks. This typically includes small business owners who employ a few individuals or run businesses on a micro scale.

Business Experience:

- The applicant must have at least 2 years of business experience in their current line of work. This ensures that the borrower has a stable business model and can generate enough revenue to repay the loan.

CNIC/SNIC:

- Applicants must have a valid NADRA-issued CNIC (Computerized National Identity Card) or SNIC (Smart National Identity Card).

Credit History:

- The applicant must have a good credit history and should not be a defaulter with Khushhali Microfinance Bank or any other financial institution.

These eligibility criteria ensure that the loan is provided to individuals who have the capacity to manage and repay it responsibly.

Loan Tenure and Repayment Options

The Khushhali Sarmaya Loan offers flexible repayment options and loan tenure, giving borrowers the freedom to choose a plan that best fits their business needs and financial situation.

Loan Tenure:

- The loan tenure ranges from 6 to 36 months (3 years). This flexibility allows businesses to repay the loan over a period that aligns with their cash flow and business cycles.

Repayment Options:

- The loan is repaid through equal monthly installments (EMI), which makes it easier for businesses to manage their finances and plan for regular, predictable payments.

This combination of flexible tenure and straightforward repayment ensures that micro-entrepreneurs can focus on running their businesses while repaying the loan at a manageable pace.

Read more : Breaking News: Punjab Green Tractor Scheme Online Registration Start

Loan Amount and Collateral Requirements

Loan Amount:

The Khushhali Sarmaya Loan offers financing between PKR 350,001 and PKR 1,000,000, depending on the size and financial needs of the business. The loan amount will be determined based on the borrower’s business capacity, revenue, and ability to repay the loan.

Collateral:

The loan offers both secured and unsecured options:

Secured Loan:

For higher loan amounts or businesses seeking lower interest rates, the loan can be secured with the following forms of collateral:

- Hypothecation of Business Stock or Machinery: The borrower can pledge business stock, plant, machinery, or other moveable assets.

- Mortgage of Land/Building: A registered or equitable mortgage on business or personal property may be required.

- Lien Marking on TDC/NSC: The borrower can pledge savings certificates or other financial assets.

- Vehicle Hypothecation (HPA): Vehicles can be pledged with the original documents retained by the bank as collateral.

Unsecured Loan:

For smaller loan amounts, the loan can be unsecured but will require:

- Personal Guarantees: A third-party guarantor is required.

- Post-Dated Cheques (PDCs): The borrower must provide post-dated cheques to secure timely repayments.

The flexibility in collateral options ensures that businesses of all sizes can access the loan, regardless of their asset base.

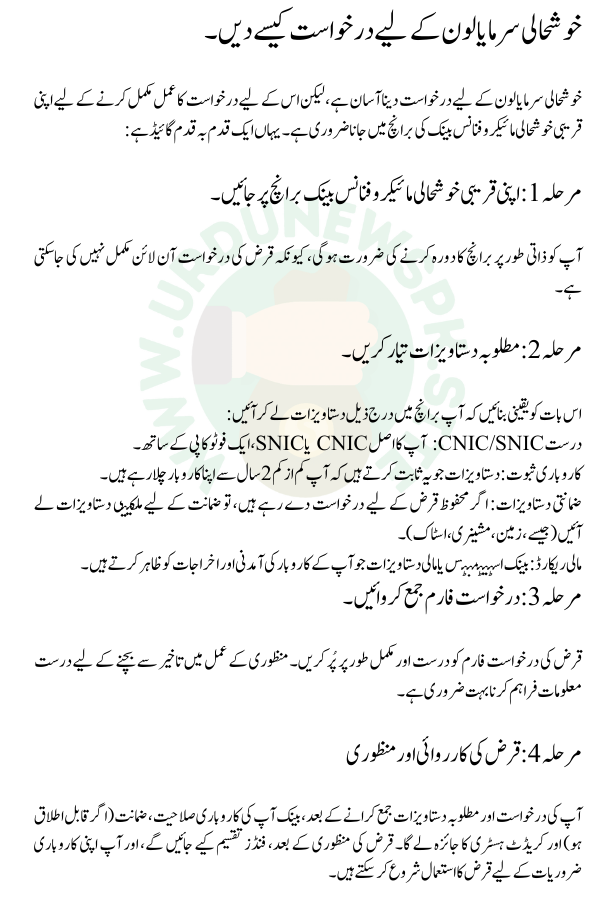

How to Apply for the Khushhali Sarmaya Loan

Applying for the Khushhali Sarmaya Loan is simple, but it requires visiting your nearest Khushhali Microfinance Bank branch to complete the application process. Here’s a step-by-step guide:

Step 1: Visit Your Nearest Khushhali Microfinance Bank Branch

You will need to visit a branch in person, as the loan application cannot be completed online.

Step 2: Prepare the Required Documents

Ensure you bring the following documents to the branch:

- Valid CNIC/SNIC: Your original CNIC or SNIC, along with a photocopy.

- Business Proof: Documents proving that you have been running your business for at least 2 years.

- Collateral Documents: If applying for a secured loan, bring ownership documents for the collateral (e.g., land, machinery, stock).

- Financial Records: Bank statements or financial documents showing the revenue and expenses of your business.

Step 3: Submit the Application Form

Fill out the loan application form accurately and completely. Providing correct information is crucial to avoid delays in the approval process.

Step 4: Loan Processing and Approval

After you submit your application and required documents, the bank will assess your business capacity, collateral (if applicable), and credit history. Once the loan is approved, the funds will be disbursed, and you can begin using the loan for your business needs.

10 Frequently Asked Questions (FAQs)

1. What is the minimum loan amount for the Khushhali Sarmaya Loan?

The minimum loan amount is PKR 350,001.

2. What is the maximum loan tenure?

The maximum loan tenure is 36 months (3 years).

3. Can I apply for the loan online?

No, you must visit your nearest Khushhali Microfinance Bank branch to apply for the loan.

4. What documents do I need to apply for the loan?

You will need a valid CNIC/SNIC, proof of business experience, and collateral documents (if applying for a secured loan).

5. What is the maximum loan amount I can apply for?

The maximum loan amount is PKR 1,000,000.

6. Is collateral required for all loan amounts?

No, collateral is not required for smaller loan amounts but is needed for larger loans or to secure lower interest rates.

7. What types of collateral are accepted?

Collateral can include business stock, machinery, land, buildings, vehicles, or savings certificates.

8. What are the repayment options?

The loan is repaid through equal monthly installments (EMIs).

9. How long does it take to get the loan approved?

The loan approval process typically takes a few working days, depending on document verification and collateral assessment.

10. Can I repay the loan early?

Yes, early repayment is allowed. However, you should check with the bank for any prepayment penalties or conditions.

Conclusion

The (Micro Enterprise Lending) Scheme 2024 is a perfect solution for micro-entrepreneurs looking to expand their businesses or manage working capital. With flexible loan amounts, repayment options, and collateral choices, this loan provides a financial lifeline for small business owners. Visit your nearest Khushhali Microfinance Bank branch today to apply and take your business to the next level!